Commercial Space Activities

- Brief Introduction

- U.S. Commercial Space Policy

- NASA’s Commercial Cargo and Commercial Crew Programs

- Other Commercial Suborbital and Orbital Vehicles, Rocket Engines

- Other Commercial Space Concepts for Earth Orbit and the Moon

- U.S. Aerospace Companies

- Major Non-U.S. Aerospace Companies

Brief Introduction

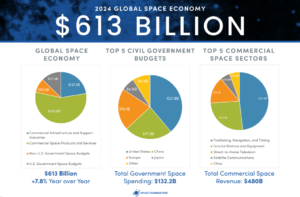

The “Space Economy”

The U.S. Space Foundation publishes an annual report with quarterly updates that tracks worldwide space spending by governments, the private sector and consumers. Detailed data are available for purchase from the Space Foundation, but The Space Report Q2 2025 puts the 2024 global space economy at $613 billion, comprised of the following segments:

- commercial infrastructure and support industries, $137.3 billion

- commercial space products and services, $343.0 billion

- U.S. government space budgets, $77.3 billion, and

- non-U.S. government space budgets, $55 billion

The European company Novaspace also publishes data about the space economy and values it at $596 million in 2024 and projects it will grow to “$944 billion by 2033, driven largely by downstream solutions leveraging satellite data.”

The Department of Commerce’s Bureau of Economic Analysis (BEA) also publishes statistics on the space economy, but only for the United States and uses a different methodology. The Space Foundation explained to SpacePolicyOnline.com that among other things “BEA takes a top-down approach, isolating space activities from broad datasets on U.S. industry outputs, while Space Foundation takes a bottom-up approach, combining specific space-related budgets and revenues to value the global space economy.”

The BEA’s June 27, 2023 report covered 2012-2021 and concluded that in 2021 the U.S. space economy accounted for “$211.6 billion of gross output, $129.9 billion (0.6 percent) of GDP, $51.1 billion of private industry compensation, and 360,000 private industry jobs.” An updated report published on June 25, 2024 concluded: “the space economy accounted for $131.8 billion, or 0.5 percent, of total U.S. GDP in 2022. Real GDP grew by 2.3 percent in the space economy, faster than growth in the overall U.S. economy (1.9 percent). The statistics also show in 2022 the space economy accounted for $232.1 billion of gross output and $54.5 billion of private-sector compensation and supported 347,000 private-sector jobs.” The March 31, 2025 edition covering 2012-2023 said: “The space economy accounted for $142.5 billion, or 0.5 percent, of total U.S. GDP in 2023. Real GDP grew by 0.6 percent in the space economy, reflecting the second consecutive year of positive real growth. The statistics also show the space economy accounted for $240.9 billion of gross output in 2023 and $57.9 billion of private-sector compensation and supported 373,000 private-sector jobs.”

Defining “Commercial” Space Activities

What makes a space activity “commercial” can be difficult to define. Some consider a commercial activity to be one in which a private sector entity puts its own capital at risk and provides goods or services primarily to other private sector entities or consumers rather than to the government. Examples of these activities would be direct-to-home satellite television (e.g. DirecTV and DishTV), satellite radio (Sirius XM), and commercial communications satellites that transmit voice, data and Internet services (such as Intelsat, SES, Eutelsat, Telesat, SpaceX (Starlink), Iridium, Globalstar and a growing number of other companies).

Other definitions are broader and include sales of consumer equipment by companies even though the satellite system is owned by the government. The chief example of this is the Global Positioning System (GPS) navigation satellite system that is owned by the U.S. Department of Defense, but has a vast array of consumer users ranging from automobile navigation systems to cell phones to precision farming. The devices used by consumers around the world in their cars, on their boats, or carried on their persons are sold by commercial companies, but the satellite signal that makes them work is provided for free by DOD.

Still broader definitions of commercial space activities include those where a company provides services primarily to government customers, such as the Boeing-Lockheed Martin United Launch Alliance (ULA) did for many years. Others do not consider these commercial because they are reliant on the government for most of their revenue and the government shoulders a major portion of the risk because the government requires the services.

In his National Space Policy issued on June 28, 2010, President Obama defined “commercial space activities” in this manner:

The term “commercial,” for the purposes of this policy, refers to space goods, services, or activities provided by private sector enterprises that bear a reasonable portion of the investment risk and responsibility for the activity, operate in accordance with typical market-based incentives for controlling cost and optimizing return on investment, and have the legal capacity to offer these goods or services to existing or potential nongovernmental customers.

President Trump retained that definition in his December 9, 2020 National Space Policy with one exception. The word “space” is omitted prior to “goods, services, or activities…”

U.S. COMMERCIAL SPACE POLICY

The government plays a major role in commercial space activities in many ways, from establishing regulatory policy, to creating policies that direct government agencies to purchase services from companies, to engaging in public-private partnerships where the government and the private sector share the risks and rewards, to traditional fixed price or cost-plus contracts for services or products.

U.S. commercial space policy is set both by presidential directive and in law. Presidential directives remain in force until and unless a future President revises them. Thus, what is in force today is a mix of directives issued by President George W. Bush (2001-2009), President Barack Obama (2009-2017), and President Donald Trump during his first term (2017-2021). President Biden (2021-2025) issued a set of national priorities in December 2021 that included commercial space and proposed commercial space legislation, but it was not acted upon by Congress.

The following summary of presidential space policies covers all space sectors for completeness. (For information on laws that affect commercial space policy, including the 2015 Commercial Space Launch Competitiveness Act, see our Space Law section.)

The most recent complete presidential National Space Policy was issued by Trump on December 9, 2020, superseding the Obama policy issued on June 28, 2010. Trump changed two sentences of the Obama policy in 2017 (see below), but the rest remained the same until the last few weeks of his administration.

Second Trump Administration (2025-present)

On August 13, 2025, President Trump issued an Executive Order on “Enabling Competition in the Commercial Space Industry” and an accompanying fact sheet. Much of the new EO is reminiscent of Space Policy Directive-3 from his first administration, calling for reforming commercial space regulations especially the “Part 450” commercial space transportation regulations that were written during his first term. He also directed the Department of Commerce to propose a process for regulating novel space activities, often referred to as “mission authorization,” a topic of debate since the Obama Administration. A new focus is spaceports, with directives to several agencies (Commerce, Defense, Transportation, Interior, NASA) to take actions to enable spaceport development.

A more comprehensive Executive Order (EO 14369) for space policy was issued on December 18, 2025, the same day Jared Isaacman was sworn in as the new NASA Administrator. He was in the Oval Office when the EO was signed along with President Trump and Michael Kratsios, Director of the White House Office of Science and Technology Policy. Ensuring American Space Superiority covers civil, national security, and commercial space policy with a strong emphasis on acquisition reform. Notably, it revokes the National Space Council and puts Kratsios in charge of implementing the EO.

Biden-Harris Administration (2021-2025)

On December 1, 2021, Vice President Kamala Harris, as chair of the White House National Space Council, released a United States Space Priorities Framework in conjunction with the first meeting of the Space Council under her leadership. It covers all aspects of space policy, including national security. Biden released an Executive Order the same day expanding the membership and duties of the Council, which supersedes the two issued by Trump in 2017 and 2020.

On April 18, 2022, Harris announced a policy that the United States will not conduct debris-generating direct-ascent antisatellite tests, sometimes called Kinetic Energy (KE) ASAT tests, and urged other countries to join the pledge. The action was in response to a Russian KE-ASAT in November 2021 that created thousands of pieces of debris that imperiled many space objects including the International Space Station.

On November 15, 2023, the Space Council released its long-awaited proposal for “mission authorization” regarding what agency or agencies are responsible for “authorization and continuing supervision” of new types of space activities by non-government entities, like companies, as required by Article VI of the 1967 Outer Space Treaty. The text of the legislative proposal is available along with a section-by-section analysis. At her third Space Council meeting on December 20, 2023, Harris released a companion “executive action” — U.S. Novel Space Activities Authorization and Supervision Framework, that the White House says will enable the Executive Branch to “prepare for and shape the future space regulatory environment.” The Space Council’s proposal was very different from what had been discussed earlier and from legislation introduced by Republicans on the House Science, Space, and Technology Committee. The committee approved the Republican bill on a partisan basis on November 29, 2023. There was no further action in the 118th Congress.

On January 16, 2025, in his final days as President, Biden issued an Executive Order on Strengthening and Promoting Innovation in the Nation’s Cybersecurity that includes cybersecurity for space systems and their supporting digital infrastructure.

Also at the White House level, the Biden-Harris Office of Science and Technology Policy (OSTP) released:

- National Research and Development Plan for Positioning, Navigation, and Timing Resilience (August 2021)

- Space Weather Research-to-Operations and Operations-to-Research Framework (March 2022)

- In-Space Servicing, Assembly and Manufacturing National Strategy (April 2022)

- United States Government Commercial Earth Observation Data Purchases: Perspectives From Earth Observations Enterprise (July 2022)

- National Orbital Debris Implementation Plan (July 2022)

- National Cislunar Science & Technology Strategy (November 2022)

- National In-Space Servicing, Assembly and Manufacturing Implementation Plan (December 2022)

- National Low Earth Orbit Research and Development Strategy (March 2023)

- National Preparedness Strategy & Action Plan for Near-Earth Object Hazards and Planetary Defense (April 2023)

- Implementation Plan of the National Space Weather Strategy and Action Plan (December 2023)

- Policy on Celestial Time Standardization in Support of the National Cislunar Science and Technology Strategy (April 2024)

- Fact Sheet: Biden-Harris Administration Announces New Actions to Advance U.S. Science and Technology Leadership in Cislunar Space (December 2024)

- Readout of the White House Microgravity Science Summit (December 2024)

- 2024 National Plan for Civil Earth Observations (December 2024)

At the agency level, Secretary of Defense Lloyd Austin issued a set of Tenets of Responsible Behavior in Space on July 7, 2021. On August 30, 2022, DOD issued a new space policy directive, DOD Directive 3100.10, Space Policy, which was updated on October 14, 2024. On April 2, 2024, DOD released its first Commercial Space Integration Strategy.

Secretary of State Antony Blinken released the first State Department Strategic Framework for Space Diplomacy on May 30, 2023.

First Trump Administration (2017-2021)

During the four years of his first Administration, Trump signed an updated National Space Policy, seven Space Policy Directives (SPDs), five space-related Executive Orders, two strategies, two reports and one National Security Presidential Memorandum (NSPM). Not all are directed at commercial space policy, but all are listed here in chronological order for completeness.

Trump used the National Space Council as the mechanism to formulate U.S. space policy, with Vice President Mike Pence as chair and Scott Pace as Executive Secretary. It met publicly five times: October 5, 2017 (at the National Air and Space Museum Udvar-Hazy Center near Dulles Airport; February 21, 2018 (at Kennedy Space Center, FL); June 18, 2018 (at the White House); March 26, 2019 (at Marshall Space Flight Center, AL); and August 20, 2019 back at Udvar-Hazy.

- Executive Order 13803, June 30, 2017, reviving the National Space Council.

- Space Policy Directive 1 , December 11, 2017, replaces two sentences of the 2010 National Space Policy regarding NASA’s human spaceflight program. It directs NASA to return humans to the lunar surface as a steppingstone to human exploration of Mars instead of an asteroid as the Obama Administration planned.

- National Space Strategy, March 23, 2018, states the strategy to implement national security, commercial and civil space policy.

- Space Policy Directive-2, May 24, 2018, takes steps towards designating the Department of Commerce as the “one-stop shop” for commercial space regulations.

- Space Policy Directive-3, June 18, 2018, establishes agency roles and responsibilities for space situational awareness and space traffic management.

- Space Policy Directive-4, February 19, 2019, proposing establishment of a U.S. Space Force as part of the U.S. Air Force.

- National Security Presidential Memorandum-20 on Launch of Spacecraft Containing Space Nuclear Systems, August 20, 2019.

- Executive Order 13905 on “Strengthening National Resilience through Responsible Use of Positioning, Navigation and Timing Services, February 12, 2020. PNT is more commonly known by the name of the DOD satellite system that provides those signals, the Global Positioning System (GPS). Other countries have similar systems, collectively referred to as Global Navigation Satellite Systems (GNSS).

- Executive Order 13906, February 13, 2020. Amending Executive Order 13803 on reviving the National Space Council.

- Executive Order 13914 on Encouraging International Support for the Recovery and Use of Space Resources, April 6, 2020, establishing U.S. policy on mining resources on the Moon and other places in the solar system, especially with regard to commercial exploration, recovery and use of such resources.

- A New Era for Deep Space Exploration and Development, July 23, 2020, laying out the Administration’s rationale for deep space human exploration.

- Space Policy Directive-5, September 4, 2020, establishing principles for space cybersecurity.

- U.S. National Space Policy, December 9, 2020, updating the 2010 National Space Policy.

- Space Policy Directive-6, December 16, 2020, National Strategy for Space Nuclear Power and Propulsion (SNPP), laying out goals, principles, and a roadmap to demonstrate the U.S. commitment to using SNPP systems “safely, effectively, and responsibly.”

- National Strategy on Planetary Protection, December 30, 2020, implementing a section of the National Space Policy on planetary protection (protecting Earth from harmful contamination by microbes from elsewhere in the solar system and vice versa).

- Executive Order 13972 Promoting Small Modular Reactors for National Defense and Space Exploration, January 12, 2021.

- Space Policy Directive-7, January 15, 2021, The United States Space-Based Positioning, Navigation, and Timing Policy, succeeding the George W. Bush Administration’s 2004 Positioning Navigation and Timing (PNT) Policy.

- Final Report on the Activities of the National Space Council: Renewing America’s Proud Legacy of Leadership in Space: Activities of the National Space Council and United States Space Enterprise, January 2021

Obama and George W. Bush Administrations

In addition to his 2010 National Space Policy, Obama issued a National Space Transportation Policy and associated fact sheet on November 21, 2013 that updated a policy issued by George W. Bush. Bush also issued a policy for commercial remote sensing satellites in 2003.

NASA’S COMMERCIAL CARGO (COTS) AND COMMERCIAL CREW PROGRAMS

NASA is engaging in the most visible examples of public-private partnerships in the space arena although the national security space program is adopting this strategy as well. While they are referred to as “commercial,” the government often provides the largest share of money for development and/or a guaranteed market.

It began with NASA’s Commercial Orbital Transportation Services (COTS) or “commercial cargo” program to develop systems to take cargo to the International Space Station (ISS), followed by the companion “commercial crew” program to ferry astronauts back and forth. The impetus for both was a decision by President George W. Bush in 2004 to terminate the space shuttle program as soon as construction of the ISS was completed. That meant NASA needed to find another way to take crews and cargo to and from ISS for the duration of its operational life. The shuttle program ended in 2011. The first commercial cargo flights began in 2012. The first operational commercial crew launch was in November 2020. In the interim, NASA paid Russia to take its crews to and from ISS.

Commercial Cargo

NASA initiated the Commercial Orbital Transportation Services (COTS) program in 2006 for the private sector to develop spacecraft and rockets to take cargo to the ISS in partnership with the government. NASA wanted to ensure competition, so signed Space Act Agreements (SAAs) with two companies, SpaceX and Rocketplane Kistler, to begin operational service to the ISS starting in 2011. Rocketplane Kistler did not meet its required milestones and NASA terminated that agreement in 2007. NASA signed an SAA with Orbital Sciences Corp. (OSC) in 2008 to replace Rocketplane Kistler.

OSC merged with ATK in 2015 and became Orbital ATK (OA). OA was acquired by Northrop Grumman in 2018 and became Northrop Grumman Innovation Systems (NGIS). After a company reorganization in January 2020, it became Northrop Grumman Space Systems (hereafter NG).

The 2011 date slipped to 2012 (SpaceX) and 2013 (NG), but both systems are now operational and the COTS program, which covered development of the systems, has ended. NASA held a press conference in November 2013 heralding its success and later released a report.

NASA now purchases cargo services from SpaceX and NG under Commercial Resupply Services (CRS) contracts. NASA initially signed contracts with each company to launch 20 tons of cargo to the ISS through the end of 2016. Contracts with both companies were later extended adding more flights to cover through 2018 and a new round of CRS-2 contracts were awarded in 2016 for later years as discussed below.

SpaceX’s cargo spacecraft is called Dragon. It is currently referred to as Cargo Dragon to distinguish it from the version that takes astronauts to space — Crew Dragon. Cargo Dragon spacecraft are launched on Falcon 9 rockets from the Space Force’s Space Launch Complex 40 (SLC-40) at Cape Canaveral, FL and NASA’s Launch Complex 39A (LC-39A) at NASA’s adjacent Kennedy Space Center. SpaceX leases those facilities from the government.

Cargo Dragon spacecraft return to Earth and splash down in the ocean. It is the only cargo spacecraft that currently services ISS capable of returning cargo to Earth. All the others — Russia’s Progress, Europe’s ATV (now discontinued), Japan’s HTV and NG’s Cygnus — are not designed to survive reentry. They burn up in the atmosphere and therefore are used for trash disposal — a less glamorous, but still critical task — and may also be used for experiments between the time they depart the ISS and reenter, which can be hours, days or weeks depending on the mission.

SpaceX conducted a test flight of the original version of Cargo Dragon to ISS in May 2012. The first operational Cargo Dragon flight took place in October 2012 and five more were successfully conducted through the spring of 2015. The seventh flight, however, failed 139 seconds after launch. The Falcon 9/Cargo Dragon combination returned to flight in April 2016 with the SpaceX CRS-8 (SpX-8) mission. The flights continue on a regular schedule, although the cadence was disrupted by an explosion at SLC-40 on September 1, 2016 that destroyed a Falcon 9 rocket and a commercial communications satellites (Amos-6) during a pre-launch test. No one was hurt, but SLC-40 was badly damaged. Launches moved over to LC-39A until SLC-40 was repaired.

SpaceX introduced a new version of Cargo Dragon (Dragon 2) on the 21st launch in December 2020. This version can dock rather than berth with ISS, and has greater payload capacity. From 2020 through 2024, Cargo Dragons landed in the Atlantic or Gulf of Mexico near their launch sites on Florida’s Space Coast instead of in the Pacific near SpaceX’s manufacturing facility in Hawthorne, CA as the original version did. However, in 2024 SpaceX announced it was moving splashdowns of all Dragons, cargo and crew, back to the coast of California beginning in 2025 in order to better control where Dragon “trunks” reenter. An unpressurized section of the capsule used for cargo, the trunk separates during descent. In the reentry profile used from 2020-2024, the trunk remained in orbit eventually falling to Earth randomly, sometimes in populated areas. By moving splashdowns back to the West Coast, they can keep it attached longer and direct it to fall harmlessly into the Pacific Ocean.

Northrop Grumman’s cargo spacecraft is Cygnus. NG typically uses its Antares rocket to launch Cygnus from the Mid-Atlantic Regional Spaceport (MARS) at Wallops Island, VA. MARS is located at NASA’s Wallops Flight Facility, but MARS itself is owned by the Commonwealth of Virginia and operated by the Virginia Commonwealth Space Flight Authority.

A test flight of Antares/Cygnus to the ISS took place in October 2013. The first operational flight (Orb-1) was launched in January 2014 and Orb-2 in July 2014. On October 28, 2014, the third mission, Orb-3, failed 15 seconds after liftoff, destroying the rocket and Cygnus, and damaging the MARS facility and surrounding area. A recovery plan was quickly announced under which it consolidated its remaining cargo requirements into four rather than five more launches using an upgraded version of Cygnus that can accommodate more cargo per flight. The failure was traced to the engine, a Russian NK-33 built four decades earlier, refurbished by Aerojet and redesignated AJ-26. The company decided to replace the NK-33/AJ26 engines entirely and use new Russian RD-181 engines for Antares instead. While waiting for the retrofit, it purchased launch services from the United Launch Alliance (ULA) for Atlas V launches of Cygnus to meet its contractual commitments to NASA. The first launch of the new version, Antares 230, was in October 2016 from Wallops.

Following Russia’s invasion of Ukraine on February 24, 2022 and the imposition of more sanctions on Russia by the United States and other countries, Russia announced it would no longer sell rocket engines to U.S. companies. Not only did Antares 230 use Russian RD-181 engines, but the first stage was built in Ukraine. NG said it had sufficient engines and first stages to fulfill its existing contract with NASA for two more flights, but needed to develop a new plan for the future. On August 18, 2022, it announced a deal with Firefly Aerospace to use Firefly Miranda engines for a new version, Antares 330. The two companies also will jointly develop a new medium-class rocket. NG bought three SpaceX Falcon 9 launches to get Cygnus to ISS while waiting for Antares 330. The final Antares 230 launched in August 2023. Two Cygnuses were launched on Falcon 9s in 2024. Another (NG-22) was scheduled for the summer of 2025, but the spacecraft was damaged during shipping to the launch site. As of August 2025, the next Cygnus is expected to launch in the fall of 2025 on the new Antares 330, recently named Eclipse.

NASA awarded a second round of commercial cargo launches (CRS-2) in January 2016. SpaceX and NG each won a minimum of six launches each and a third company, Sierra Nevada Corporation (SNC), was added also with six launches of its Dream Chaser spacecraft that resembles a small space shuttle. In 2021, SNC spun off Sierra Space as a separate entity. The first launch of Dream Chaser was expected in the first half of 2024 on ULA’s new Vulcan rocket, but was delayed and didn’t take place in 2024. As of August 2025, no schedule has been announced for that flight.

Commercial Crew

President Obama proposed a dramatic change to the U.S. human spaceflight program in his FY2011 budget request to Congress, released on February 1, 2010. He proposed relying on the commercial sector instead of NASA to build and operate systems to take people to and from low Earth orbit (LEO). That includes taking NASA astronauts to and from the ISS. He requested $6 billion over 5 years (FY2011-2015) in NASA’s budget to subsidize companies to develop “commercial crew” launch vehicles and spacecraft for LEO missions.

He also proposed cancelling the Constellation program, begun under President George W. Bush, for NASA to build new launch vehicles (Ares I and V) and a spacecraft (Orion) to take astronauts back to the Moon and on to Mars, as well as to and from ISS. He wanted NASA to spend several years investing in “game-changing” technologies before deciding on what systems to build and where to go.

The lack of a specific destination and timetable for these “beyond-LEO” human spaceflight missions made his proposal especially unpopular and on April 15, 2010, he elaborated on his plans in a speech at NASA’s Kennedy Space Center in Florida. At that time he made clear that he saw no need for U.S. astronauts to return to the Moon, but landing people on Mars remained the eventual goal, and he said he expected that to happen in his lifetime. Meanwhile, he wanted NASA to focus on sending astronauts to an asteroid by 2025 as his initial beyond-LEO destination, and send them to orbit (but not land on) Mars in the 2030s.

Congressional Reaction. The proposal was very controversial and vigorously debated in Congress. The 2010 NASA Authorization Act (P.L. 111-267), signed into law in October 2010, was a compromise wherein NASA was directed to develop its own crew space transportation system — the Space Launch System (SLS) and a Multi-Purpose Crew Vehicle (MPCV) — as well as fund commercial crew. The law required that the space transportation system also be able to function as a backup for commercial crew in case those systems did not materialize or if they failed. NASA selected the Orion spacecraft that was being developed in the Constellation program as the MPCV, so the system now is usually referred to as SLS/Orion.

President Obama’s FY2012 budget request for NASA, released in February 2011, was similarly controversial because the congressional committees that oversee NASA believed it contravened the compromise reached in the 2010 NASA Authorization Act. NASA requested more money than was authorized in the 2010 Act for commercial crew and less than was authorized for SLS/Orion. The tense relationship between Congress and the Obama Administration lasted for several years, wherein Congress made clear that SLS/Orion was the priority, not commercial crew, adding money for SLS/Orion and not providing as much as requested for commercial crew.

For FY2011, FY2012, and FY2013, Congress provided sharply less funding than the Administration requested. The request for FY2013 was $830 million, for example, but Congress approved only $525 million. The request for FY2014 was $821 million and Congress approved $696 million. Though it was $125 million less than the request, it was more than the agency received in the past and the percentage cut was less, leaving many commercial crew advocates happy with the result. The request for FY2015 was $848 million and in a sign of continued thawing of relationships, Congress approved $805 million. The request for FY2016 was $1.244 billion and Congress appropriated that amount. FY2016 was the peak funding year for commercial crew and for FY2017, the request of $1.185 billion began the downward trajectory. Congress approved the requested amounts.

With the termination of the space shuttle program in July 2011, NASA could not launch astronauts to the ISS until the commercial crew systems were operational. Initially this “gap” between the end of the shuttle program and the availability of commercial crew services was expected to last four years, but the first commercial crew flight did not take place until 2020, almost exactly a nine-year gap.

The SpaceX crewed flight test, Demo-2, with NASA astronauts Doug Hurley and Bob Behnken was successfully accomplished from May 30-August 2, 2020. (Demo-1 was an uncrewed test flight in March 2019.) The system then was certified by NASA as operational for its needs and the first operational flight, Crew-1, launched in November 2020.

While waiting for the commercial crew systems, NASA purchased crew transportation services from Russia at a cost that rose to a high of $90 million per seat. NASA intends to continue launching astronauts on Russia’s Soyuz, and Russia to launch cosmonauts on the U.S. systems, to ensure all are trained to fly on all the vehicles, but on a no-exchange-of-funds basis. This “crew exchange” or “seat swap” agreement was signed in July 2022 despite the tense geopolitical situation stemming from Russia’s invasion of Ukraine. NASA’s Frank Rubio launched on Soyuz MS-22 on September 21, 2022 and Russian cosmonaut Anna Kikina on Crew-5 on October 5, 2022. Kikina is the only woman in Russia’s cosmonaut corps. She returned with Crew-5, but Rubio ended up staying for just over a year with his Soyuz MS-22 crewmates because of a problem with the spacecraft that necessitated its replacement by Soyuz MS-23. Russian cosmonaut Andrey Fedyaev was on Crew-6, Konstantin Borisov on Crew-7, Alexander Grebenkin on Crew-8, Aleksandr Gorbunov on Crew-9, Kirill Peskov on Crew-10, and Oleg Platanov on Crew-11. NASA’s Loral O’Hara flew to ISS on Soyuz MS-24, Tracy Caldwell-Dyson on Soyuz MS-25, Don Pettit on Soyuz MS-26, and Jonny Kim on Soyuz MS-27.

Evolution of the Commercial Crew Program. NASA initially awarded contracts to five companies for Crew Transportation Concepts and Technology Demonstration, or CCDEV (commercial crew development) in February 2010: Blue Origin, Boeing, Paragon Space Development Corp., Sierra Nevada Corp., and United Launch Alliance. Another round of winners of the CCDEV2 competition was announced in April 2011: Blue Origin, Boeing, Sierra Nevada, and SpaceX. Those contracts were awarded as Space Act Agreements (SAAs) where NASA can pay companies for meeting agreed-upon milestones, but has less oversight or insight into what the companies are doing compared with traditional contracts. NASA planned to adopt traditional procurement methods under the Federal Acquisition Regulations (FAR) for the next phase of commercial crew development — specifically, fixed price contracts — but changed course in December 2011 because of budget uncertainties in future years that it concluded made fixed price contracts unrealistic at that time.

The CCDEV program transitioned into the Commercial Crew Integrated Capability (CCiCAP) program for the commercial companies to develop an integrated crew transportation system (spacecraft, launch vehicle, and ground systems). In August 2012, NASA selected “2 1/2” proposals, meaning it fully funded two companies (SpaceX and Boeing) and partially funded a third (Sierra Nevada Corporation, or SNC). SpaceX’s Crew Dragon capsule is described above. Boeing is also developing a capsule, CST-100 Starliner. As noted above, SNC’s Dream Chaser, is a winged vehicle that resembles a small version of the space shuttle. In fact, it is based on a NASA design (HL-20) for an ISS crew rescue vehicle that the agency cancelled in the 1990s.

On September 16, 2014, NASA awarded FAR-based fixed price contracts for the final phase of the commercial crew development program, Commercial Crew Transportation Capability (CCtCAP). It chose Boeing and SpaceX, with Boeing receiving $4.2 billion and SpaceX receiving $2.6 billion. Sierra Nevada filed a protest of the awards on September 26, 2014 with the Government Accountability Office (GAO) saying there were “serious questions and inconsistencies in the procurement process.” Consequently, NASA issued a stop-work order to Boeing and SpaceX for the CCtCAP contracts, but later rescinded it. Sierra Nevada filed a lawsuit against the government for that decision, but a judge verbally indicated she would not overturn it. GAO denied Sierra Nevada’s protest. As described above, SNC currently is focusing on providing cargo services using Dream Chaser and won an award under the CRS-2 contract.

The names “commercial cargo” and “commercial crew” imply that the systems are being built at the expense of the private sector, but the companies are supported by taxpayer dollars. NASA spent about $800 million on the COTS commercial cargo program for system development and continues to pay separately for services. The commercial crew CCtCAP awards to SpaceX and Boeing are for a total of $6.8 billion of taxpayer money. How much the companies themselves invested in development is proprietary information and neither NASA nor the companies say how much they are spending except for Boeing including its losses on Starliner as part of its quarterly earnings statements.

At a September 2012 congressional hearing, NASA’s then-Associate Administrator for Human Exploration and Operations Bill Gerstenmaier conceded that the government was paying 80-90 percent of the costs for the development of the commercial crew systems, but a more current figure is not available. On the other hand, both companies have had to pay themselves to fix problems like recovering from SpaceX’s 2019 explosion and Boeing’s troubles with Starliner.

It is more accurate to refer to these as public-private partnerships (PPPs) than commercial activities, and the PPP terminology is, in fact, being used more often as NASA extends this acquisition model to other activities like the Human Landing Systems for the Artemis program to return astronauts to the Moon (described below).

Commercial Crew Flights Begin. SpaceX and Boeing continued to develop their systems. Each was required to fly an uncrewed test flight followed by a crewed test flight before NASA certifies them for operational use.

SpaceX successfully conducted its uncrewed test flight, Demo-1, in March 2019, but the capsule was destroyed the next month during preparations for an In-Flight Abort (IFA) test. SpaceX successfully conducted the IFA test in January 2020, paving the way for the 2020 crewed test flight, Demo-2, and subsequent operational flights for NASA as well as non-NASA private astronaut flights. As of July 23, 2025, SpaceX had launched 11 Crew Dragons with people aboard for NASA (Demo-2 and Crew 1-10) and seven private astronaut non-NASA Crew Dragons as discussed below.

Boeing attempted its uncrewed Orbital Flight Test (OFT) of the CST-100 Starliner on December 20, 2019. The launch aboard an Atlas V rocket was successful, but the Atlas V leaves Starliner in a suborbital trajectory. Starliner’s own engines must take the spacecraft the rest of the way to orbit and to the ISS. A software problem set Starliner’s Mission Elapsed Timer (MET) to the wrong time and left the spacecraft with too little propellant to reach ISS. It landed two days after launch. During those two days, Boeing engineers seeking to find the problem with the MET discovered a separate software failure that could have proved catastrophic during landing. They fixed it just in time and landing was successful. Because the launch and landing were successful, NASA and Boeing initially painted a positive picture of the test despite its inability to perform rendezvous and docking operations with ISS. However, the post-flight investigation showed troubling failures at Boeing and the decision was made to refly the OFT before attempting the crewed flight test. Because this is a fixed price contract, Boeing must pay for the additional test. In January 2021, Boeing and NASA set March 25, 2021 as the launch date for OFT-2, but that slipped to July and then to August 3. Boeing had to scrub the launch about two hours before liftoff because 13 propulsion valves would not open. The launch was postponed to sometime in 2022. OFT-2 finally successfully flew in May 2022.

The Crew Flight Test was next. On November 3, 2022, NASA announced another delay, from February to April 2023, and in June 2023, Boeing delayed it indefinitely due to newly discovered problems. By October 2022, Boeing had had to pay almost $900 million of its own money for Starliner because it is a fixed price contract and in July 2023 revealed it had another $257 million loss on the program.

In August 2023, Boeing said the Crew Flight Test would take place no earlier than March 2024. It finally launched on June 5, 2024 with two NASA astronauts, Butch Wilmore and Suni Williams, both experienced astronauts and Navy test pilots, for what was intended to be an 8-day test flight. However, during the one-day trip to the ISS, Starliner experienced problems with the propulsion system. After weeks of tests in space and on the ground, NASA concluded it did not have sufficient confidence in the system to risk the astronauts’ lives and decided to leave Wilmore and Williams aboard the ISS and bring Starliner back to Earth empty. It successfully landed on September 6, 2024.

Williams and Wilmore were integrated into the next regular crew exchange as part of Crew-9 and returned with them on March 18, 2025 amidst considerable misinformation about why they remained aboard (they were never “stranded,” they were waiting for their replacements on Crew-10 to arrive) and whether SpaceX’s Elon Musk and the Trump White House “rescued” them. (In fact, their return was delayed a few weeks because SpaceX’s new Crew Dragon wasn’t ready to launch Crew-10 and they had to switch to another capsule. The new Crew Dragon, Grace, finally flew with Axiom-4 in June 2025).

Boeing and NASA continue to investigate what went wrong and what’s needed to fix Starliner. Boeing has spent at least $2 billion of its own money on Starliner in addition to the $4.2 billion contract with NASA. During a July 2025 news conference prior to the launch of Crew-11, NASA officials said they are looking at another Starliner launch early next year and it may carry only cargo, not crew.

Boeing’s performance is being criticized in comparison to SpaceX, which now routinely launches crews not only for NASA, but other customers. It’s important to remember, however, that Crew Dragon’s first launch was four years later than planned. Commercial crew advocates place the blame on Congress because it provided less-than-requested funding in the early years. That is correct for FY2011-FY2014, but since FY2015 the request was essentially fully funded, undercutting that argument. One of the goals of using a commercial approach was to save time and money over traditional government procurements, so it is difficult to say if that was a success.

Non-NASA Commercial Crew Missions. Another goal was for the commercial crew companies to find non-NASA customers and SpaceX is demonstrating success on that score. As of August 2025, SpaceX has five reusable Crew Dragon capsules: Endeavour, Resilience, Endurance, Freedom, and Grace available.

In September 2021, an all-commercial crew of four flew the Inspiration4 mission, spending three days in Earth orbit. Jared Isaacman, the wealthy entrepreneur who paid an undisclosed price for the entire mission, subsequently announced he purchased another three SpaceX missions, two on Crew Dragon and the third on the first human spaceflight of SpaceX’s Starship, which is still in development.

Isaacman calls them the “Polaris” missions. He said on October 3, 2022 that the first, Polaris Dawn, would launch no earlier than March 1, 2023 and include the first commercial spacewalk, or extravehicular activity (EVA). That date was extremely optimistic and soon slipped to 2024. The five-day mission successfully began on September 10, 2024. Isaacman and crew member Sarah Gillis, a SpaceX engineer, conducted the first commercial spacewalk two days later by standing in the open hatch of the spacecraft for several minutes each.

President-elect Donald Trump announced plans to nominate Isaacman to be the next Administrator of NASA in December 2024 and formally submitted the nomination on January 20, 2025. Isaacman said at the time the next two Polaris flights “may end up on hold for a little bit.” However, Trump withdrew Isaacman’s nomination in May 2025 after a falling out with Elon Musk. Musk spent more than $250 million on Trump’s election campaign and was a close advisor for several months after the November 2024 election. He recommended Isaacman as NASA Administrator. Musk and Trump clashed over provisions in Trump’s One, Big Beautiful Act (OBBA, H.R. 1), however, and parted ways with Isaacman’s nomination one of the casualties. Isaacman’s current plans for another Polaris mission and a flight on Starship are unknown. Starship is discussed below.

On September 29, 2022, Isaacman, SpaceX and NASA revealed they were conducting a study, at no cost to NASA, on the feasibility of sending the second Polaris Crew Dragon to dock with the Hubble Space Telescope and boost its orbit and perhaps do other life-extension activities. Hubble was launched in 1990, but astronauts on five space shuttle missions replaced much of the hardware and all the instruments so it is not as old as the calendar would suggest. Its orbit is slowly deteriorating due to atmospheric drag, however, and needs a boost to keep operating far into the future. NASA rejected the proposal.

Separately, Axiom Space has purchased at least four Crew Dragon flights. Unlike the Isaacman flights, these visit the International Space Station for several days of joint operations. The first, Axiom-1, took place in April 2022. The four-person crew, all private astronauts but one a retired NASA astronaut, spent almost twice as long in space as planned because poor weather in the splashdown area prevented their return.The crew was commanded by former NASA astronaut Michael López-Alegria. The other three were wealthy men from the United States, Canada, and Israel. The price per seat has not been disclosed, but is rumored to be $55 million apiece. Russia has taken a number of tourists to the ISS (see below), but this was a first for the United States. All the ISS partners (the United States, Russia, Canada, Japan, and 11 European countries) must agree to whoever will visit the ISS.

Axiom-2, in May 2023, was commanded by former NASA astronaut Peggy Whitson who also now works for Axiom. Joining her was race car driver John Shoffer and two Saudi government astronauts, Rayyanah Barnawi and Ali Alqarni, from what is now the Saudi Space Agency. Barnawi became the first Arab woman in orbit. (She was not the first Arab woman in space, however, a distinction that belongs to Sara Sabry who was a passenger on a Blue Origin suborbital flight in August 2022). The first Saudi to fly in space was Sultan bin Salman Al Saud on the 1985 U.S. space shuttle mission STS 51-G.

Axiom-3 launched on January 18, 2024 with López-Alegria again in the commander’s seat. He was joined by three military pilots from Sweden, Turkey, and Italy: Marcus Wandt, Alper Gezeravci, and Walter Villadei. Gezeravci is the first Turkish astronaut. They were to spend 14 days on ISS, but landing again was delayed because of bad weather. López-Alegria is a dual citizen of Spain and the United States so they called Axiom-3 the first all-European spaceflight. Wandt was selected as a European Space Agency reserve astronaut, but the Swedish government decided to arrange for him to fly to ISS with Axiom rather than wait for an opportunity through NASA. Poland is doing the same thing. ESA selected a new group of astronauts in 2023: five “career” astronauts who immediately went into ESA’s training program, 11 in the “reserve” corps, and one with a physical disability.

Axiom-4 launched on June 25, 2025 with Axiom’s Whitson, ESA reserve astronaut Sławosz Uznański (Poland), Shubhanshu Shukla (India), and Tibor Kapu (Hungary). They got to fly on a brand new Crew Dragon — the fifth in the series — that they named Grace. At the last minute their launch was delayed for almost two weeks as NASA assessed the success of repairs made to air leaks in the Russian segment of ISS. They had to remain in quarantine all that time. They were expected to spend 14 days on the ISS, but got to stay a little longer and returned on July 15.

Separately, Axiom made a deal with NASA to fly an astronaut from the United Arab Emirates to the ISS for a routine 6-month crew rotation. Sultan Alneyadi was part of Crew-6. He, Barnawi and Alqarni were on ISS together, the first time three Arabs have been in space at the same time.

A completely separate private astronaut flight in March 2025 put four astronauts in orbit around Earth’s poles for the first time. Financed by cryptocurrency billionaire Chun Wang, the Fram2 crew spent three days in space aboard Crew Dragon Resilience.

One additional note since Presidents sometimes like to take credit for successful ideas even though they predate their tenure, commercial cargo was a Bush Administration initiative and well underway by the time President Obama took office. Commercial crew was an Obama Administration initiative and well underway by the time President Trump took office the first time in 2017.

OTHER COMMERCIAL SUBORBITAL AND ORBITAL VEHICLES, ROCKET ENGINES

Suborbital

Suborbital rockets do not go into orbit around Earth, but fly to a high altitude and provide several minutes of microgravity when returning to Earth. They have been commonly used throughout the space age in the United States and elsewhere around the world for experiments that need minutes, but not hours or days, of microgravity. Historically, government agencies have been the providers of these services and also are users along with academic institutions and others.

Today, however, two companies offer suborbital rides not only for payloads, but passengers: Richard Branson’s Virgin Galactic with SpaceShip Two and Jeff Bezos’s Blue Origin with New Shepard.

There is no legal definition of where air ends and space begins. Virgin Galactic and the FAA use 80 kilometers (50 miles), but the Federation Aeronautique Internationale (FAI), which certifies air records, uses 100 kilometers (62 miles) as that boundary — the “Kármán line” named after Theodore von Kármán. That was the altitude Burt Rutan’s Scaled Composites had to achieve with SpaceShipOne to win the Ansari X-Prize and is what Blue Origin uses for New Shepard flights.

Branson formed Virgin Galactic in 2004 to take anyone with the requisite funds (the pricetag initially was $250,000, but has risen since) on suborbital flights using SpaceShipTwo (SS2), a derivative of SpaceShipOne (SS1). Designed and built by Burt Rutan’s Scaled Composites, SS1 won the Ansari X-Prize on October 4, 2004 (the anniversary of the launch of the world’s first satellite, Sputnik, by the Soviet Union in 1957) by flying SS1 above the Kármán line twice within two weeks.

The spaceship is taken aloft by an aircraft, the Mothership, then detaches, fires its rocket engine to ascend and briefly cross the imaginary line between air and space, then glides back to land on the same runway from which it departed. The entire trip takes about one hour.

Branson’s original plan was to build five SS2 vehicles. During a test flight on October 31, 2014, however, the only existing SS2 vehicle was destroyed in an accident that killed co-pilot Michael Alsbury and seriously injured pilot Peter Siebold. The National Transportation Safety Board (NTSB) investigated the accident, concluding it was co-pilot error, but criticizing the spacecraft’s design that made such an error possible. Scaled Composites, later part of Northrop Grumman, was in charge of building SS2 and the two pilots were Scaled employees.

Virgin Galactic took over construction of the vehicle from Scaled and a second SpaceShipTwo craft, Unity, began flying. (The Mothership aircraft is named Eve after Branson’s mother.) The company achieved a milestone in December 2018 when two pilots flew SS2 above 80 kilometers (50 miles), which some consider the dividing line between air and space (see above). On February 22, 2019, it achieved another milestone when two pilots were joined by another Virgin Galactic employee, Beth Moses, on a second flight above 80 kilometers. Moses is the company’s Chief Astronaut Instructor and the first woman to make a spaceflight on a commercially-developed space vehicle. On July 11, 2021, Branson himself flew over the 50-mile threshold with other Virgin Galactic employees (including Moses on her second flight).

The company said they would make their first commercial flight two months later, but instead paused all flights for almost two years — an “enhancement period” — to make modifications after tests indicated problems with the strength margins of certain materials. The next flight didn’t take place until May 2023 with only company employees onboard. The first revenue-producing commercial flight, Galactic-01, finally flew in June 2023, 19 years after Branson founded the company.

Four more revenue-producing flights flew in 2023, but the company announced in November 2023 it would stop flying Unity after just two or three more flights in 2024 and wait until an upgraded Delta version is ready. Delta can carry additional passengers and fly more frequently and thus will be more profitable. A test flight of Delta is planned for 2025 and revenue-producing flights in 2026. The company immediately began laying off employees. The last flight of Unity was Galactic-07 in June 2024.

Blue Origin uses the Kármán line as the dividing line between air and space. Owned by Amazon.com billionaire Jeff Bezos, Blue Origin’s reusable, suborbital rocket is New Shepard, is just that — a rocket. It lifts off from a launch pad in West Texas, ascends above the Kármán line, the capsule detaches from the rocket and both land separately back on Earth after about 10 minutes. It is named after Alan Shepard, the first American to reach space on a suborbital flight in 1961.

Blue Origin flew 15 test flights, some carrying scientific payloads for NASA, before the first flight with passengers on July 20, 2021, the anniversary of the Apollo 11 landing on the Moon. Bezos himself, along with his brother, Mark, famed aviatrix Wally Funk, and a German teenager, Oliver Daemen, make the approximately 10 minute flight up across the 100 kilometer mark and back down to the Texas desert. Daemen was the first paying passenger, but the price was not disclosed. Blue Origin had conducted an auction for the first seat on New Shepard and the high bid was $28 million. Oddly, the person who won the auction paid the money (which Bezos distributed to groups involved in STEM education) but decided not to fly at that time. He kept his identity secret until December 2021 when he revealed himself to be Justin Sun, a cryptocurrency entrepreneur. He ultimately flew on New Shepard-34 in August 2025.

Blue Origin began a regular cadence of passenger flights, one of which took Star Trek actor William Shatner to space for real instead of a Hollywood studio, but New Shepard flights were suspended for more than a year after a September 12, 2022 failure. No people were aboard that time, only scientific experiments. Blue Origin provided very little information about what happened. FAA closed its investigation into the failure in September 2023 and the return-to-flight mission took place successfully in December 2023. Once again only experiments, not people, were aboard. Flights with passengers resumed in 2024.

NASA Suborbital Human Spaceflights. In 2020, NASA announced an interest in flying people on suborbital vehicles like SpaceShipTwo or New Shepard either as part of astronaut training or scientists who want to conduct experiments. In October 2020, it selected Alan Stern as the first person to fly under this new “SubC” program. Stern is a planetary scientist at the Southwest Research Institute (SwRI) perhaps best known as the Principal Investigator of the New Horizons mission that flew past Pluto. NASA last flew people on suborbital flights in the 1960s with the Mercury and X-15 programs. Stern did not want to wait, however, and flew on a Virgin Galactic mission in November 2023. He and SwRI stressed he still will fly on a NASA-sponsored mission later.

Orbital

Escaping Earth’s gravity well and getting into orbit is much more difficult than suborbital flight, but a number of companies are developing such systems to launch satellites and other payloads with mixed success. The following discussion highlights only a few.

Apart from SpaceX, the most successful so far is Rocket Lab, a U.S.-based company founded and led by New Zealander Peter Beck. It originally launched only from New Zealand’s Mahia Peninsula, but now also has pads at the Mid-Atlantic Regional Spaceport at NASA’s Wallops Flight Facility in Virginia. The small Electron rocket launches from both sites. The new, larger Neutron will launch from Wallops.

Rocket Lab was one of three companies to get NASA contracts in October 2014 for “Venture Class” launch services to place very small satellites (cubesats, microsats, and nanosatellites) in orbit. Rocket Lab has had many successful launches of its Electron rocket and in July 2022 sent a spacecraft beyond Earth orbit for the first time, NASA’s CAPSTONE, which is orbiting the Moon. NASA is only one of Rocket Lab’s many government and private sector customers.

The other two were Virgin Galactic and Firefly Space Systems.

Virgin Galactic created Virgin Orbit as a separate part of Branson’s Virgin Group to develop the air-launched LauncherOne. Virgin Orbit’s LauncherOne failed during its first test flight in May 2020, but had a few successful launches after that and was planning to offer services around the globe. However, a failure during its first international launch in January 2023 from the United Kingdom led to bankruptcy. It ceased operations in May 2023.

Firefly filed for Chapter 7 bankruptcy in April 2017, but is making a comeback. Its Alpha rocket finally made its first partially successful trip to orbit in October 2022 from Vandenberg Space Force Base, CA and a fully successful flight a year later — the Victus Nox mission for the U.S. Space Force that demonstrated rapid launch capability. As discussed above, Firefly is developing a larger rocket, Eclipse, together with Northrop Grumman. Firefly also is building lunar landers for NASA’s CLPS initiative (discussed elsewhere on this page).

Blue Origin is building New Glenn for Earth orbiting missions. At one time it was planning a much bigger rocket, New Armstrong, to send payloads to the Moon, but that hasn’t been mentioned recently. The rockets are named after the U.S. astronauts who first reached orbit, John Glenn, and the Moon, Neil Armstrong. After years of delays, New Glenn had its first launch in January 2025. The first stage is reusable and designed to land on a barge in the Atlantic. On this flight, the second stage reached orbit as planned, but the first stage did not successfully land. They plan to try again in August 2025.

Blue Origin builds its own rocket engines. New Glenn’s first stage uses BE-4 engines with liquified natural gas as fuel. The United Launch Alliance (ULA) also uses BE-4 engines for its new Vulcan rocket, which will replace the Atlas V. The first launch of Vulcan successfully took place on January 8, 2024, and the second in October 2024.

SpaceX founder Elon Musk is well known for his interest in creating a “multi-planet species” by sending a million people to inhabit Mars as a “backup plan” in case Earth is destroyed by natural or human-caused events. He also is interested in missions to the Moon. In March 2017, he announced he would send two people around the Moon in 2018 in a Dragon capsule launched by his Falcon Heavy rocket. The Falcon Heavy made its first flight on February 6, 2018, but the day before Musk announced that he had decided against human-rating the Falcon Heavy and instead focus on using his next rocket, then called the Big Falcon Rocket (BFR), for human spaceflight.

In September 2018, Musk announced that a Japanese billionaire, Yusaku Maezawa, had purchased the first BFR flight around the Moon, planned for 2023. Maezawa decided to try out spaceflight closer to home and visited the International Space Station on a Russian Soyuz spacecraft in December 2021 and in 2024 decided against the Moon trip.

Musk renamed BFR as Starship. The first stage is “Super Heavy” or “booster” and the second stage, for crew or cargo, is “Starship” or simply “ship.” Confusingly, the combination is also referred to as Starship.

Musk is conducting tests of Starship at Starbase near Boca Chica, TX (near Brownsville). Starship will be used for many types of missions, not only putting satellites and people in earth orbit, but sending cargo and crews to the Moon and beyond. As discussed below, NASA selected the Starship Human Landing System (HLS) for its first crew return to the Moon, Artemis III, planned for 2027, as well as Artemis IV.

As of July 23, 2025, Starship is still in development having flown nine uncrewed Integrated Flight Tests (IFTs) with mixed success. On IFT-5, IFT-7, and IFT-8, the enormous “Super Heavy” first stage returned to the launch tower to be caught by mechanical arms called “chopsticks” in an impressive display of technological prowess. But the “catch” was not successful on IFT-6 and not attempted on IFT-9 because SpaceX was doing tests associated with reuse of the booster. On IFT-7 and IFT-8 the second stage — Starship — exploded over the Caribbean Ocean. On IFT-9 in May 2025, it got further, but SpaceX had to destroy the vehicle over the Indian Ocean after a propulsion failure put it into a spin.

COMMERCIAL SPACE CONCEPTS FOR EARTH ORBIT AND THE MOON, INCLUDING NASA’S ARTEMIS PROGRAM

Commercial Space Stations

Perhaps the first concept for a U.S. commercial space station was advanced by Robert Bigelow, owner of Budget Suites of America hotels, but was later abandoned. He worked for several years on using expandable modules (often referred to as “inflatable,” but the correct term is expandable) and launched two subscale prototypes —Genesis I and Genesis II — on Russian rockets in 2006 and 2007 respectively. In January 2013, NASA signed a $17.8 million contract with Bigelow Aerospace to add one of his modules to the International Space Station (ISS). The Bigelow Expandable Activity Module (BEAM) was launched to the ISS in 2016 on the SpaceX CRS-8 (SpX-8) flight and expanded in May 2016. Bigelow’s structures trace their roots to NASA’s cancelled Transhab project, which was intended to provide crew quarters on the ISS using such a module. BEAM is a small prototype. At one point, Bigelow wanted NASA to attach a full size B330 module to the ISS in 2020, a concept he called XBASE, but never pursued that. In fact, in December 2021, Bigelow transferred title and ownership of BEAM to NASA, abandoning Bigelow’s space aspirations.

NASA opened a Broad Agency Announcement (BAA) for the NEXT Space Technologies for Exploration Partnerships-2 (NEXTStep-2) in 2016 to solicit ideas for space habitats and Bigelow was one of six companies selected along with Boeing, Lockheed Martin, Orbital ATK (now Northrop Grumman), Sierra Nevada, and Nanoracks.

Nanoracks was best known for arranging transportation for very small satellites (cubesats) to be delivered to the ISS for deployment into orbit. Its participation in NEXTStep-2 was a new venture and it teamed with Space Systems Loral (later Maxar Technologies) and launch services company ULA to create the Ixiom concept. ULA’s Atlas V rocket has an upper stage named Centaur. The Ixiom concept would have converted Centaur upper stages into habitats. America’s first space station, Skylab, was a converted upper stage for the Saturn V rocket, although it was never used as an upper stage. It was modified into a space station before launch. The Ixiom concept was not pursued, however, and should not be confused with Axiom Space that is building a commercial space station module and flying astronauts to the ISS. Nanoracks moved on to develop the commercial Bishop Airlock that is attached to ISS to make it easier to deploy cubesats. Now part of Voyager Space, Nanoracks also is one of the companies developing concepts for Commercial LEO Destinations (CLDs) for NASA.

NASA’s Commercial LEO Destinations (CLDs). Recognizing that the International Space Station will not last forever, NASA is facilitating companies to build their own space stations in low Earth orbit (LEO) so NASA can be just one of many customers buying whatever services it needs rather than owning the facility. Through the CLD program, NASA hopes at least one commercial space station will be available by 2030 when the ISS is expected to be deorbited.

NASA contracted with 13 companies in 2018 to conduct studies of a potential LEO commercial space station economy, but results released in May 2019 painted a questionable outlook about the expected market for such services. In June 2019, NASA announced new policies intended to entice companies to get into the CLD business, including opening more commercial opportunities on ISS such as allowing space tourists to visit as a forerunner to entirely commercial operations later, with a price list of what they must pay for services like life support. The prices do not include transportation to get to and from ISS, which a customer would have to arrange with one of the commercial crew providers. NASA updated the pricing policy in May 2021.

But getting commercial companies to build their own space stations is another matter and NASA is pursuing Public-Private Partnerships (PPPs) as it is in other projects. NASA requested $150 million in FY2020, but Congress allocated only $15 million. It repeated its $150 million request in FY2021, but received only $17 million because Congress was not convinced NASA’s plan was sufficiently mature.

Nonetheless, in January 2020 NASA awarded a contract to Axiom Space, led by former NASA ISS Program Manager Mike Suffredini, that had a plan to build out a commercial space station by first attaching modules to the ISS and then separating them to operate as a free-flying facility, Axiom Station.

NASA chose three more companies in December 2021 to design commercial space stations that did not involve the ISS. Blue Origin partnered with Sierra Space and others; Nanoracks partnered with Lockheed Martin and others; and Northrop Grumman partnered with Dynetics and others. These space stations would exist as free-flying space stations from the outset.

Northrop Grumman withdrew in October 2023 and joined the Nanoracks/Voyager Space effort instead, called Starlab. Europe’s Airbus is also a partner in Starlab. The Blue Origin/Sierra Space space station is called Orbital Reef.

As of August 2025, the three CLD efforts receiving funding from NASA through Phase I of the program are:

- Axiom Station. Axiom revised its assembly sequence in December 2024 so its modules could separate from ISS earlier than the original plan because of production delays.

- Starlab. Voyager Technologies (formerly Voyager Space) in partnership with Airbus and others.

- Orbital Reef. Blue Origin in partnership with Sierra Space, Boeing, Redwire and others.

Congress warmed up to the commercial LEO concept, providing NASA $101 million in FY2022, $224 million in FY2023, and $228 million in FY2024. The FY2025 request was $170 million. NASA is operating under a full year Continuing Resolution for FY2025 and the amount allocated for CLD is not specified. The FY2026 request is $272 million.

NASA approved an acquisition strategy for Phase 2 of the program in December 2024, but on August 4, 2025, Acting NASA Administrator Sean Duffy issued a memo substantially changing the acquisition approach because of anticipated funding shortfalls and the need to have at least one CLD operational by the time the ISS is deorbited in 2030. FAR-based firm fixed price contracts no longer will be awarded for Phase 2. Instead, funded Space Act Agreements will be used to provide companies more flexibility. NASA no longer is requiring that the CLDs be capable of continuous occupancy by 4-person crews. Now the CLDs can be “crew-tended,” with 4-person crews remaining for one month at a time. Previously the CLDs had to be certified by NASA in Phase 2, but NASA postponed that to a future phase.

Other Commercial Space Station Concepts

Several other commercial space station concepts are under consideration or in development.

- Vast’s Haven-1 and Haven-2

- ABOVE:Space’s Prometheus

- Gravitics’ StarMax

- Sierra Space’s Large Integrated Flexible Environment (LIFE) and

- Think Orbital’s ThinkPlatform-3

NASA signed unfunded Space Act Agreements with seven companies in 2023 through the Collaborations for Commercial Space Capabilities-2 initiative, which “is designed to advance commercial space-related efforts through NASA contributions of technical expertise, assessments, lessons learned, technologies, and data.” Not all of them are related to commercial space stations, but Vast, Sierra Space, and ThinkOrbital are on that list.

Vast, which is partnering with SpaceX, says it will launch its first space station, Haven-1, in 2026. The small space station will launch on a SpaceX Falcon 9 rocket. A SpaceX Crew Dragon with four crew members will dock with it and remain for two-weeks. SpaceX’s Starlink satellite system will provide communications. A more capable multi-modular Haven-2 is planned. The first module would launch in 2028 and be completed in 2032, supporting a crew of 12.

Commercial Space and the Artemis Program to Return Astronauts to the Moon

In March 2019, NASA was directed by the first Trump Administration to return humans to the lunar surface by 2024, four years earlier than NASA was planning based on Trump’s 2017 Space Policy Directive-1. The program is named Artemis after Apollo’s twin sister in Greek mythology. (See our Civil topic for more information.)

The Biden Administration continued Trump’s Artemis program. At first they kept 2024 as the date when astronauts would return to the Moon, but acknowledged in November 2021 that it would not take place until 2025. In January 2024 they pushed the landing to September 2026 and in December 2024 to mid-2027.

The short deadline imposed in 2019, however, shaped NASA’s approach to accomplishing the goal, with a strong focus on commercial as well as international partnerships.

NASA’s overall concept (“architecture”) initially was to launch astronauts in Orion crew capsules aboard Space Launch System (SLS) rockets to a small space station, Gateway, in a “Near Rectilinear Halo Orbit” or NRHO around the Moon. There the astronauts would transfer to a Human Landing System (HLS) to get down to and back from the surface. Once back at Gateway, they would return to Earth in Orion.

The architecture was challenged by some experts as too complicated. NASA later decided the Gateway was not “mandatory” to get astronauts on the Moon by 2024, but insisted it will be needed after that to support “sustainable” operations on the lunar surface. Gateway remains part of the plan.

NASA owns SLS and Orion (Boeing and Lockheed Martin, respectively, are the prime contractors), but is acquiring the Gateway and HLS through commercial and international partnerships.

NASA does not want to own the HLS systems, but to purchase services from companies just as it now buys commercial cargo and commercial crew services to ISS. That concept was controversial and legislation introduced in 2019 in the House would have required the government to own the HLS systems. The bill never proceeded beyond subcommittee markup, however, and the 2022 NASA Authorization Act does not include that requirement. But it does direct NASA to develop criteria “for determining whether NASA should make, manage, or buy key capabilities within the Program or engage with international partners to access such capabilities.” It further directs that only government astronauts may carry out Artemis human lunar landing missions including surface and in-space activities.

NASA’s Gateway Lunar Space Station. Eventually Gateway will be composed of modules and other components from NASA, Canada, Japan, the United Arab Emirates, and ESA.

The initial version, however, will be only the Power and Propulsion Element (PPE) and the Habitation and Logistics Outpost (HALO).

NASA signed a firm fixed-price contract with Maxar Technologies, which builds communications satellites (formerly the Space Systems Loral unit), for the PPE wherein it would build and launch the PPE and own it for one year after launch for an in-space flight demonstration. NASA then would have the option to buy it. The PPE will be outfitted with much larger than usual solar panels that could provide 50 kilowatts (kw) of power for a solar-electric propulsion (SEP) system enabling Gateway to change its orbit around the Moon to meet various scientific objectives.

NASA signed a sole-source contract with Northrop Grumman for HALO, which is based on the design of the company’s Cygnus commercial cargo spacecraft, which is built by Europe’s ThalesAlenia Space. In July 2023, Northrop Grumman reported a $36 million loss on the HALO fixed price contract.

Originally PPE and HALO were to be launched separately and dock once in lunar orbit. However, NASA changed its mind in the spring of 2020 and now plans to integrate PPE and HALO together on Earth and launch them on a single rocket, a SpaceX Falcon Heavy.

As Gateway evolves, Canada will supply a robotic arm, Canadarm3, similar to those it built for the space shuttle and ISS. ESA will build the European System Providing Refueling, Infrastructure and Telecommunications (ESPRIT) refueling module and, with Japan, an iHAB international habitation module. At one time NASA hoped Russia, another ISS partner, would provide an airlock, but Russia showed little interest and after Russia’s invasion of Ukraine in February 2022, NASA began looking at alternatives. In January 2024, NASA announced that the United Arab Emirates will provide the airlock. The UAE signed a contract with ThalesAlenia Space to build the Emirates Airlock in February 2025.

SpaceX won the first Gateway logistics contract in 2020 to take supplies to the lunar space station.

The second Trump Administration, however, wants to cancel Gateway entirely. In July 2025 the Senate Appropriations Committee reported its Commerce-Justice-Science (CJS) bill that funds NASA, fully supporting Gateway, however. The 2025 reconciliation bill (H.R. 1, the One, Big Beautiful Bill Act) also funds Gateway.

NASA Human Landing Systems (HLS). NASA originally planned to build the HLS systems using traditional contracts where it would be the owner. Its notional design comprised three stages: a Transfer Vehicle to reach a lower orbit around the Moon than is possible with Orion or the Gateway; a Descent Vehicle to reach the surface; and an Ascent Vehicle to return to Gateway.

After the 2019 directive to get people back on the Moon by 2024, however, NASA decided to procure the HLS systems through Public-Private Partnerships hoping to accelerate the process and leaving the design to the companies proposing to build them. On April 30, 2020, NASA awarded 10-month study contracts to three bidders: a Blue Origin-led “national team” with Lockheed Martin, Northrop Grumman, and Draper; SpaceX; and Dynetics, which had a number of partners including Sierra Nevada.

Blue Origin’s bid was the only one resembling NASA’s three-stage concept: transfer vehicle, lander, and ascent vehicle. Blue Moon was the lander. Lockheed Martin would provide the ascent vehicle based on Artemis’s Orion. Northrop Grumman would provide the transfer vehicle based on Cygnus. Dynetics proposed a two-stage concept. SpaceX proposed a one-stage concept, Starship, although many Starship launches are required to accomplish the entire mission because it must be refueled at a depot in Earth orbit. Quick descriptions of the three designs are available in an April 30, 2020 SpacePolicyOnline.com article. The companies spent their own money in addition to the NASA awards ($579 million to Blue Origin, $253 million to Dynetics, and $135 million to SpaceX) on the concept studies.

At the time, NASA was committed to returning astronauts to the lunar surface in 2024, though many were skeptical that could be achieved. As noted earlier, some in Congress objected to the entire concept of allowing the private sector to own the landers. More importantly, congressional appropriators provided only 25 percent of the funding NASA requested for FY2021 to proceed with HLS development.

NASA thinks it imperative to have two HLS contractors to ensure competition and redundancy, but the cut in funding in FY2021 meant NASA could choose only one. In April 2021, NASA selected SpaceX, prompting protests from Blue Origin and Dynetics to the Government Accountability Office, which denied the protests in July 2021. Blue Origin then sued NASA in federal court, but also lost.

The Biden Administration supported the 2024 goal, but as noted earlier the date slipped. NASA still insisted that having at least two companies was crucial. In 2021 it opened a Lunar Exploration and Transportation Services (LETS) solicitation for landings after Artemis III (the first time astronauts would land on the Moon), but changed its mind and awarded a second HLS service contract to SpaceX for Artemis IV (which originally was not going to involve a landing).

For Artemis III, Starship HLS will dock directly with the Orion spacecraft, but beginning with Artemis IV, Starship HLS will dock with the Gateway and the astronauts will transfer from Orion into Starship through the Gateway.

For landings after Artemis IV, NASA opened a new Sustaining Lunar Development solicitation in March 2022. In its quest for a second supplier, it was open to any company except SpaceX. Blue Origin’s Blue Moon lander won a contract for Artemis V, so there now are two HLS suppliers.

Although NASA promotes a vision of sustainable, long-term lunar exploration and utilization, then-NASA Administrator Bill Nelson said in 2022 that NASA itself plans only one landing per year over about 10 years. It is using the lunar missions only as a “proving ground” before sending people to Mars. Whether a sufficient commercial and international market will develop to support multiple HLS providers remains to be seen, one of the risks for companies in Public-Private Partnerships.

The second Trump Administration, however, wants to cancel SLS and Orion after Artemis III and shift to commercial vehicles instead. None exist at the moment, however, raising concerns in Congress, which is determined to stay ahead of China, which is plannign to begin sending taikonauts to the Moon in 2030. China, Russia and other countries plan to build an International Lunar Research Station (ILRS) on the Moon.The 2025 reconciliation bill funds SLS and Orion through Artemis V.

Non-NASA Commercial Human Lunar Excursions. SpaceX plans Starship flights to Earth orbit, the Moon and Mars separate from its contracts with NASA. As noted earlier, in 2018 Japanese billionaire Yusaku Maezawa bought the first Starship flight around the Moon, but changed his mind in 2024. Maezawa had bought the entire flight of that Starship and chose companions to join him. In October 2022, Dennis Tito and his wife bought just two seats on the second Starship trip around the Moon, opening what SpaceX calls airline-like passenger travel where people can buy only the number of seats they want instead of the whole capacity.

Robotic Lunar Landers and NASA’s Commercial Lunar Payload Services (CLPS) Initiative. Even before the 2019 directive to accelerate the human return to the Moon by four years, NASA established a Public-Private Partnership for companies to build and launch small robotic lunar landers that will precede astronauts as well as work in tandem with them for lunar exploration — the Commercial Lunar Payload Services or CLPS initiative.

Through CLPS, NASA is only buying services. The companies develop and launch the landers on their own. NASA provides only science and technology experiments to be placed on the landers and money, expecting the companies to find other customers to close the business case.

The failures in 2019 of small lunar landers built by Israel’s SpaceIL (Beresheet) and the Indian Space Research Organisation (Vikram) underscored how difficult it is to successfully land on the Moon. NASA officials said they realized the difficulty and will be satisfied if only 50 percent of the CLPS missions succeed, calling it “taking shots on goal.”

NASA awarded Indefinite Delivery Indefinite Quantity (IDIQ) CLPS contracts to nine companies in 2018 and five more in 2019 to deliver NASA payloads to the lunar surface. All are eligible for task order assignments.